ADVERTISEMENTS:

The following points highlight the eight main types of cost in microeconomics. The types are: 1. Opportunity Cost 2. Real Cost 3. Short-Run and Long-Run Costs 4. Fixed Cost 5. Variable Cost 6. Total Costs 7. Average Cost or Average Total Cost 8. Marginal Cost.

Type # 1. Opportunity Cost:

Opportunity cost is concerned with the cost of forgone opportunities. The concept of opportunity cost focuses attention on the net revenue that could be generated in the next best use of a scarce input. Since this net revenue must be given up, or sacrificed, to make the scarce input available for the best use, it is called opportunity cost of the input. Alternatively, opportunity cost of producing a commodity is the cost of the foregone alternatives.

Significance of the Opportunity Cost:

ADVERTISEMENTS:

The concept of opportunity cost is very significant in economic analysis because of scarcity of resources. It helps economists to know how to allocate these limited resources in different branches of production.

For instance, an economy can produce more wheat by sacrificing production of some other commodity, say rice. This concept is so important in the use of factors of production and helps in equality of payment of factor incomes to equally efficient factors. For example, an industry must pay wages which are at least equal to what is being paid in other industries otherwise labor will leave the industry and avail the next best possible opportunity.

Type # 2. Real Cost:

Real costs refer to the payments which are made to the factors of production to compensate for the efforts involved in rendering their services. These are, in fact, a measure of the risk, disutility and discomfort experienced by the factor in the course of the productive activity.

Type # 3. Short-Run and Long-Run Costs:

The short-run is defined as a period in which the supply of at least one of the inputs cannot be changed by the firm. For example, certain inputs like machinery, buildings etc. cannot be changed by the firm whenever it so desires. It takes time to replace, add or dismantle them. In the short- run some inputs are fixed while the others are variable.

ADVERTISEMENTS:

The latter kind of input gives those costs that vary with the degree of utilization of variable input. The short-run costs are, therefore, of two types- fixed costs and variable costs. The fixed costs remain unchanged, while variable costs fluctuate with output.

The long-run, on the other hand, is defined as a period in which all inputs can be varied as desired. That is, in adjustments and changes are possible to realize. Long-run costs are cost that can vary with the size of plant and with other facilities normally regarded as fixed in the short-run. In fact, in the long run there are no fixed inputs and, therefore, no fixed costs, i.e., all costs are variable.

Thus, both short-run and long-run are relative concepts with no definite time limits. These are defined on the basis of the nature of costs incurred by the firm. The short-run is that time period in which at least one or more of the factors of production is fixed so that the cost incurred on it remains constant throughout this time period. In the long-run, however, all the factors of production become variable and there are no fixed costs.

Type # 4. Fixed Cost:

Fixed costs are the costs which do not change with changes in the volume of output during the short period. These are primarily incurred on fixed assets such as machines, buildings etc. Production may come down to zero or maximum, the fixed costs remain unaffected. In other words, the costs incurred, during a production process, on the fixed factors of production are referred to as fixed costs of production. The fixed costs are also called supplementary costs, overhead costs, indirect costs etc.

Type # 5. Variable Cost:

ADVERTISEMENTS:

Variable costs are the cost which varies with changes in the volume of output. Such costs increase when output increases and vice-versa. These are also called direct costs (because they change directly with change in the level of output) and prime costs. Examples of such costs are cost of raw materials, transport charges, fuel, power, wages etc.

Total Variable Cost depends on the number of units produced in the firm. There exists direct relationship between total variable cost and the firm’s output. At zero level of output, the variable costs are zero and the cost varies according to varying in output.

Type # 6. Total Costs:

Total cost refers to the total expenditure done by a business concern in order to carry out a certain production activity. In other words, total cost is the total expenditure incurred in the production of a given quantity of a commodity. It is the sum of the total fixed costs (TFC) and total variable costs (TVC) borne by the firm. Also, it is the sum of the explicit and implicit costs of the firm.

Explicit costs are the contractual payments actually made by a firm for purchasing or hiring the services of factor inputs. These costs are included while computing the expenses of a firm. Implicit costs are the opportunity cost of the use of factors which a producer does not buy or hire but already owns. The term imputed costs is also used for the same.

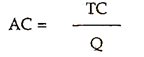

Type # 7. Average Cost or Average Total Cost:

ADVERTISEMENTS:

Average cost is the cost per unit of output assuming that production of each unit of output incurs the same cost i.e.

AC = TC / Number of Units

ADVERTISEMENTS:

There are three major types of Average Cost.

They are:

(i) Average variable cost,

(ii) Average fixed cost and

(iii) Average total cost.

(i) Average Variable Cost:

Average Variable Cost is the per unit total variable cost of production i.e.

(ii) Average Fixed Cost:

Average Fixed Cost is the per unit total fixed cost. It is determined by dividing the total fixed cost by the units produced.

(iii) Average Total Cost:

Average cost is obtained by dividing the total cost by the number of units produced i.e.

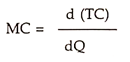

Type # 8. Marginal Cost:

Marginal costs are defined as the addition made to the total cost when an additional unit of the output is produced. It is the incremental or additional cost incurred when there is addition to the existing output of goods and services.

For example, if the total cost increases from Rs. 2,000 to Rs. 2,100 when production increases from 10 units to 11 units, the marginal cost of 11th unit is:

Rs. 2,100 — Rs. 2,000 = Rs. 100.

Hence, the marginal cost for the (n+1)th unit is the difference between the total costs for producing (n+1) units and the total costs for producing n units, i.e.

MC = TC n +1 — TC n.

Alternatively, marginal cost is the change in the total cost resulting from a unit change in output.

Features of Marginal Cost:

The following are the important features of Marginal Cost:

1. Marginal cost deals with unit-by-unit changes.

2. Marginal cost is the amount added to total cost by a unit increase in output.

3. Marginal cost as a concept is particularly superior to incremental cost when dealing with decisions like:

i. Selecting optimum level of outputs,

ii. Selecting least cost combination of inputs,

iii. Selecting optimum cost combination of inputs,

iv. Selecting optimum maturity of productive assets.

Diagrammatic Representation of Marginal cost:

Marginal cost is defined as the additional cost incurred when an additional unit of the commodity is produced. In other words, it is the net addition to the total cost given a unit change in the output.

Marginal cost is a U-shaped curve as shown in the Figure 10.6. This is because of the three stages of production (increasing, constant and decreasing) in which the three laws of costs operate. Initially, costs increase at a diminishing rate causing marginal cost to fall. After marginal cost reaches its minimum point, cost increase at an increasing rate, causing marginal cost to rise indefinitely.

Interrelationship of Total, Average and Marginal Cost:

We can see-the interrelationship of Total cost (TC), Average cost (AC) and Marginal cost (MC) in the Figure 10.7. But before analyzing these costs diagrammatically, it is appropriate to see this interrelationship through the schedule (see Table 10.1.).

An Interrelationship Schedule of TC, AC and MC:

Interrelationship Diagram:

The interrelationship of Total cost, Marginal Cost and Average cost can also interpret with the help of a diagram.

The Figure 10.7 depicts the relationship among total cost, average cost and marginal cost which can be explained as:

(1) In the initial stages of production, marginal cost is a falling curve due to the law of diminishing costs. Hence, total cost increases at a diminishing rate. Average cost is also a falling curve during this period but average cost falls at a gradual pace and lies above marginal cost.

(2) Once the law of increasing costs sets in, total cost rises at an increasing rate and marginal cost starts to rise. But average cost continues to fall for some more time till it reaches at minimum point, where it meets marginal cost.

(3) After reaching its optimum point, average cost starts to rise. But the rise in marginal cost is after that of the average cost. Hence, the marginal cost lies above average cost. Total cost continues to increase at an increasing rate throughout the production process. The Table 10.1 illustrates the relationship between these three parameters.

Comments are closed.